Mergers & Acquisitions | A Banner Year for Plastics & Packaging Sectors

- Published: December 06, 2015, By Rick Weil, Mesirow Financial

Global deal-values in 2015 have already topped the record books, surpassing the all-time annual record of $4.1 trillion set in 2007.

The year 2015 has been a banner one for mergers and acquisitions (M&A) in the plastics and packaging sectors and related segments. Global M&A has been driven to record heights this year, in part, as the return of the mega-deal boosted global deal values. Private equity (PE) firms have taken an active and leading role in reshaping areas of the packaging and plastics markets.

The year 2015 has been a banner one for mergers and acquisitions (M&A) in the plastics and packaging sectors and related segments. Global M&A has been driven to record heights this year, in part, as the return of the mega-deal boosted global deal values. Private equity (PE) firms have taken an active and leading role in reshaping areas of the packaging and plastics markets.

In today’s market, however, private equity firms are feeling pressure from increasingly competitive corporate acquirers and high valuation levels or target companies. Strategic acquirers also remain active due to their significant cash reserves, internal and external pressure to grow earnings, and limited organic growth options, among other factors.

In a business environment where costs have already been reduced over the past several years and companies are struggling to achieve growth, M&A can provide a viable pathway for expansion. The changing economic environment has compelled some leading companies to diversify their product portfolios, expand their sales channels and geographic reach, in many cases through acquisitions.

Global deal-values in 2015 have already topped the record books, reaching $4.2 trillion as of late-November and surpassing the all-time annual record of $4.1 trillion set in 2007. US-targeted M&A activity, which accounts for nearly half of global M&A volume, has had a record setting year as well. As of mid-November, M&A targeting American companies stood at $2.03 trillion, a 55% increase from the $1.3 trillion announced through the same period last year. The gains have been driven by a surge of “mega” deals (mergers and acquisitions that are greater than $5 billion in value), which account for 47% of all activity—the highest proportion since 1999.

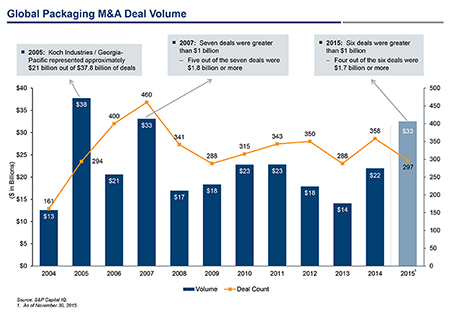

As can be seen in the chart below [view larger chart], M&A activity in the plastics and packaging sectors remains robust. $32.5 billion in deals have been announced globally through November, this is up 179.2% from $11.6 billion for same period last year. This also includes a number of mega-deals, such as Rock-Tenn Co.’s $10.9 billion merger with MeadWestvaco Corp. (nka: WestRock Co.) and Ball Corp.’s acquisition of Rexam plc for $8.7 billion.

Purchase price multiples have remained comparatively high in 2015. Plastics and packaging M&A multiples increased to an average of 8.6x trailing EBITDA in the first half of 2015, compared with an average of 8.3x during 2014. M&A multiples are approaching the levels seen in the 2007 peak, which may be pushing sellers to consider deals.

In today’s competitive M&A market, PE firms have, in many cases, been forced to pay higher purchase prices in order to “put money to work.” PE firms are sitting on record levels of “dry powder” (committed-but-uninvested capital), as pension funds, endowments, and sovereign wealth funds increase their allocations to private equity. Pension funds in particular are benefiting from the superior returns that private equity consistently provides to their funds. Private equity delivered a 12.3% annualized return to the median public pension over the past 10 years, more than any other asset class.

By comparison, the median public pension received a 7.5% annualized return on its total fund during the same period. However, given recent market volatility and an increasingly competitive deal-making environment, private equity firms may face increased difficulty in achieving appropriate returns in the coming years.

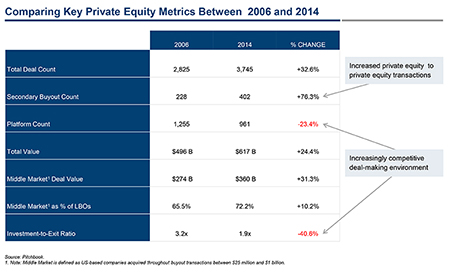

With these high levels of dry powder and high expectations for above average returns, private equity firms are feeling the pressure to invest. This pressure, combined with a limited supply of attractively priced targets in the marketplace, has prompted PE firms to turn to other financial sponsors to find possible transactions. As such, secondary buyouts, or private equity-to-private equity transactions, have increased 76.3% from 2006 to 2014. Additionally, we’ve seen a decline in private equity investment-to-exit ratio from 3.2x to 1.9x over the same period.

As multiples continue to climb, private equity firms have been exiting portfolio companies in record volumes in an effort to lock in solid returns. However, as exit activity and secondary buyout count remain elevated, PE firms may face a decreased number of opportunities for portfolio company value maximization, limiting future return potential. [view larger chart]

Private equity firms have maintained a very healthy interest in the plastics and packaging industries largely because these sectors are viewed as lower risk and less cyclical than other sectors of the economy. The use of leverage in a highly cyclical environment, such as the capital goods industry for example, can be risky. However, given that packaging is driven by the food, beverage, and personal care industries, the cash flows are much more reliable and consequently more suitable to a private equity capital structure.

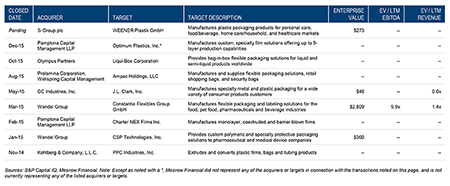

Some recent notable private equity investments in plastics and packaging include: [view larger chart]

There has also been a notable trend of strategic companies outside of the plastics and packaging sectors such as Quad/Graphics Inc., Transcontinental Inc. and R.R. Donnelley making acquisitions of plastics and packaging companies in order to diversify and expand their product portfolios away from secularly challenged markets like commercial printing. For example, Transcontinental Inc. has recently completed acquisitions of Capri Packaging Inc., a supplier of printed flexible plastic packaging products, and Ultra Flex Packaging Corp., a printer, laminator, and converter of flexible packaging.

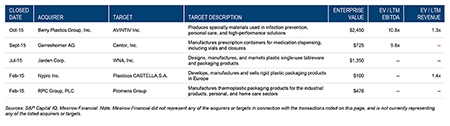

There are also a number of active strategic acquirers within the plastics and packaging sectors that have been expanding through M&A. The table below highlights notable strategic deals. [view larger chart]

There are plenty of reasons to expect packaging M&A to remain active into 2016. M&A continues to be a viable strategy for packaging executives as a result of tepid organic growth coupled with a favorable financing environment and large cash reserves. Private equity firms should also remain busy in the packaging and plastics space as they seek to deploy their growing levels of available capital. With both strategic acquirers and financial sponsors on the trail for acquisitions, packaging M&A activity is likely to remain elevated through the remainder of this year and into 2016.

ABOUT THE AUTHOR

Rick Weil is a managing director in Mesirow Financial’s Investment Banking Group. He is responsible for leading deal teams on middle-market M&A transactions and developing the firm’s relationships with plastics, packaging, and specialty printing clients. Since joining the firm in 2000, Rick has been involved in more than 100 M&A transactions in the rigid and flexible packaging, labels, folding cartons, specialty printing, tissue, and corrugated packaging sectors. He serves family businesses, publicly traded corporations and private equity firms alike.

Prior to joining Mesirow Financial, Rick was a manager in the Ernst & Young Transaction Services Group in Chicago. Spanning his 15 years of investment banking experience, Rick has been featured in industry-leading publications such as Plastics Today and Plastics News. In addition, he has been a guest speaker at numerous conferences and events including the 2015 Western Plastics Assn. Annual Conference, Plastic News’ Financial Summit, Executive Forum and Caps and Closures conferences, as well as the Assn. for Visual Packaging Manufacturers Pack Expo and the Fall Executive Conference for the Flexible Packaging Assn.